Affluence Investment Fund 2018 Review

What a difference 12 months makes! At the end of 2017 markets were soaring and investors were enjoying the easy money that was being made (it always feels easy on the way up). Now, at the end of 2018 investors are not so relaxed. Most major markets recorded losses for the year after a brutal last quarter sell off, with little indication of whether markets recover or continue to fall from here.

The Affluence Investment Fund recorded its first annual loss in 2018 (albeit small), after achieving strong returns in the previous three years. Obviously not the result we would like, however a normal part of investing. The past three months has seen elements of panic at time on behalf of investors, with indiscriminate selling in some areas. One of the most important things to do in times of heightened volatility is to remain rational. Unfortunately, many investors buy when markets are rising and the outlook is rosy, only to worry and sell when markets fall.

While we don’t know if markets will increase or decrease in the short term, we do know they are cheaper (and thus offering better value) than they were in the middle of 2018. The intrinsic value of assets (equities, property, fixed income assets) is generally fairly stable. However, the share price or traded value of these assets can vary dramatically both higher and lower. For the patient investor, this is a tremendous opportunity.

As markets fell over the past three months, we continued to add to investments where we see the best value. Long term investing success is a marathon, not a sprint, and we spend little time focusing on short term performance results. If we can take advantage of bouts of volatility to buy more attractively priced investments, than the long-term returns will take care of themselves.

Objectives and Philosophy

As a reminder, the investment objective for the Affluence Investment Fund is to provide investors with the following:

- A minimum distribution yield of 5% per annum, paid monthly.

- A total annualised return (distribution plus increase in unit price) of at least inflation plus 5% over rolling 3 year periods.

- Access to a diversified portfolio of underlying investments.

- Volatility or returns which is less than half that of the ASX200 Index, measured over rolling 3 year periods.

Our performance benchmark is a tough target. In order to achieve this return target in the current environment the following competing factors need to be balanced:

- It is important to preserve capital and limit the impact of market falls.

- A relatively large allocation to growth assets is required, on average.

- Cash and government bonds have, and continue to provide very low returns.

As always in investing, it comes down to a balance between risk and return. If we become too fixated on avoiding potential losses, vastly reduce our growth investments allocation and hide in cash, we know we are virtually guaranteed not to achieve our performance target.

The Fund needs to have enough exposure to potentially higher returning growth assets to achieve the target return. Of course, these growth assets also have the largest probability of price fluctuations. Over the long-term equities should be expected to produce total returns of 8-10% per annum. Along the way, equity markets can produce dizzying highs and terrifying lows. In the past 10 years annual returns for the ASX200 Index have ranged from negative 38% to positive 37%.

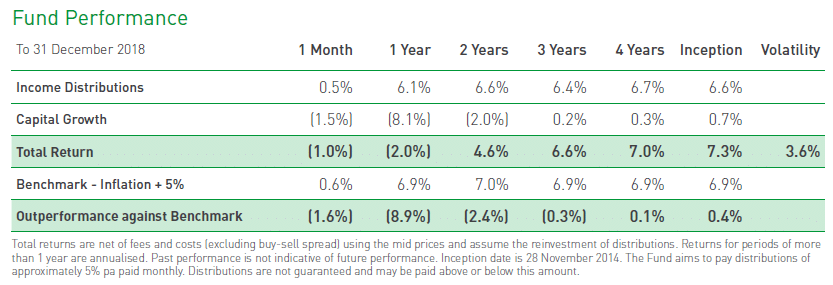

Our job is to find an appropriate balance between these two competing forces. The result is a portfolio that we believe can achieve our return target, while reducing the impact of market falls. However, reducing the impact of drawdowns doesn’t mean they can be avoided, and the Fund recorded a loss of 2.0% for 2018. While no one likes losing money, it must be remembered that negative return periods are an entirely normal part of the investment cycle.

Affluence Investment Fund Performance

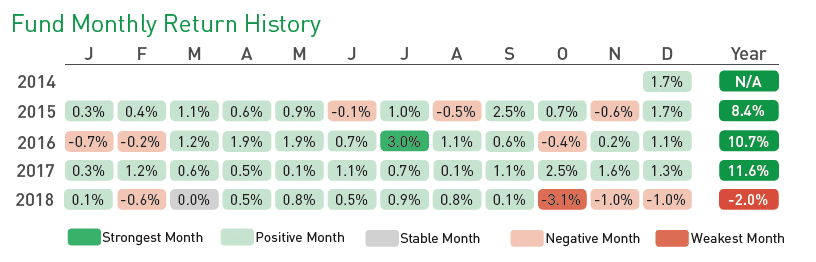

Our monthly performance since inception in December 2014:

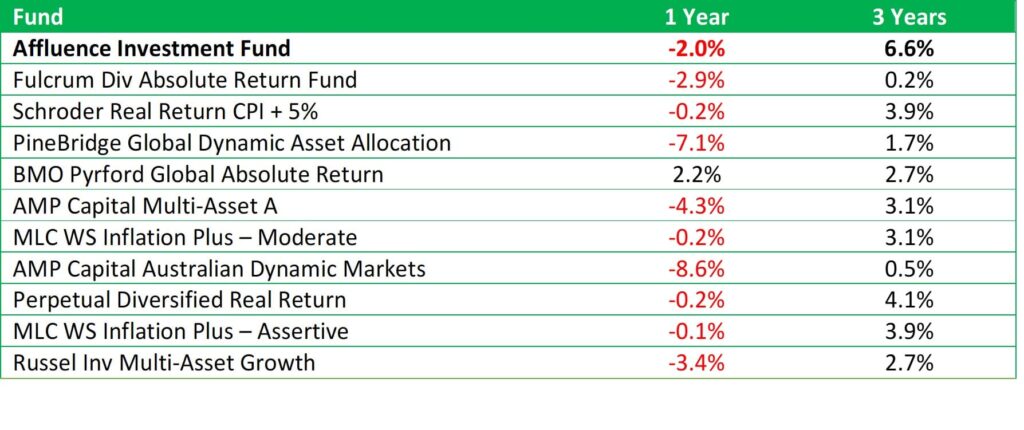

Our performance against the ten largest funds in our investment sector:

The past 12 months was the Fund’s first negative calendar year. The first quarter of the year started relatively strongly, with the Fund performing well during the initial global market correction in March 2018.

Markets bounced back fairly quickly and went on to hit new highs (all time highs in the US) later in the year. During that middle part of the year when equity markets were performing strongly, the Fund was posting modest positive returns, but not as high as equity markets. This was due to the Fund’s diversified asset allocation, our view that most asset classes were expensive and the portfolio’s value style bias. This could best be categorised as a period where those assets which were already very expensive got even more so. For example, the growth investment style significantly outperformed value investing, and technology shares continued to soar.

Finally, global markets plummeted during the last quarter. The Fund saw its worst three monthly returns ever during that period, however it still fell significantly less than most markets and most similar funds. It was a very difficult period to navigate, with very few places to hide.

There is no doubt that 2018 was a tough market all around, the last quarter particularly. We have included a selection of major market returns for 2018 below. In comparison, and given the conditions, the Affluence Investment Fund fared reasonably.

Most importantly, our long-term performance remains strong, with the Fund returning 7.3% per annum since inception, outperforming our benchmark of 6.9% per annum and the ASX 200 of 6.1% per annum.

Below we have provided additional detail on performance for various sectors of the portfolio.

Equities

Pleasingly, both the Affluence LIC Fund and our global equities investments recorded small positive returns for the 12 months, outperforming the relevant market benchmarks.

Less pleasing, the major contributor to the negative result in 2018 was our Australian equities exposure, which underperformed the ASX 200 Index for the year.

The disappointing 2018 leads to the obvious question of why we hold a reasonably high level of equites exposure? Over the longer term, equities are one of the highest returning asset class. They are also one of the most volatile, which results in the large variance between negative and positive years.

The Affluence Investment Fund is a multi-asset fund. It will never be fully invested in just equities but it is likely it will always have a substantial exposure to them. Over the longer term we are certain this will produce superior returns. As investors we must accept the short-term volatility that accompanies it. We rely in part on our other investments to help cushion the impact of negative years in stock markets.

Our poor Australian equities return in 2018 was mostly due to a combination of our biases towards the value investment style and small cap stocks. As the index results above suggest, a number of our managers that invest in value and smaller companies had particularly poor years in 2018. This significantly detracted from the Fund’s performance.

Value has underperformed growth substantially over the past few years, despite strong evidence from various studies that value investing outperforms in the long term. By some measures, the gap in performance between the two styles is as wide as it has ever been. We are increasingly positioned for a return to more normal conditions, and a resurgence in value investing returns in the future.

There was a stark difference in performance in 2018 between the larger companies of the ASX 200 Index (-2.8%), and the smaller stocks in the ASX Small Ordinaries Index (-8.7%) and the ASX Emerging Companies Index (-19.9%). We tend to always have more exposure to smaller and emerging companies, because over time active managers in this space can produce higher investment returns. And as prices fell, we invested more with managers who are active in this space.

We only invest with managers who are benchmark unaware and who we assess as having a genuine chance of outperforming over the long term. This by necessity means they produce returns that can be very uncorrelated with the major indexes. While that gives them a good chance at winning in the long term, the accompanying risk is that they can have periods where they underperform, sometimes significantly. That doesn’t mean they’ve forgotten how to make money, just that they’re doing things differently.

In many cases, we increase our allocation to managers who maintain an impressive long term track record but have had a recent run of bad form. We do this where we believe there is a good chance they can outperform significantly in the medium term. A lot of our value and small company managers now meet that test, and their portfolios look very inexpensive.

Alternatives

As asset valuations continued to increase during 2018, we continued to expand our alternatives portfolio. As at 31 December 2018 this sector accounted for 16.2% of the Affluence Investment Fund over 9 investments.

Alternative means different things to different investors. We define alternatives as investments whose returns are not dependent on those of major equities, property and bond markets. Examples include market neutral strategies, event driven strategies, global macro strategies, and futures strategies. The key characteristic of all these strategies is that they don’t rely on markets just going up to make money. This can make them a useful portfolio addition when valuations are elevated and there is an increased risk of market declines.

Over the longer term, we would not expect these strategies to generate as high returns as equities. However, we expect them to produce returns well above cash. All else being equal, if growth asset valuations continued to fall and reach (or go below) fair value, we would expect to decrease our allocation to alternatives and increase our allocation to growth assets.

Our alternatives portfolio did not perform as well as we would have liked in 2018, recording a small negative return. The reasons for this are different for each investment, however the continuing low levels of sustained volatility, despite two significant market corrections, was a very significant factor. We are still very confident of each of our existing managers in this space and continue to allocate to them. The portfolio is well diversified by manager, strategy and asset class.

In 2018, with the benefit of hindsight, it would have been better to have held fewer alternatives, and to instead have relied more upon the more traditional defenders of wealth, being cash and high quality bonds. Given the current forward return prospects for cash and bonds, we do not believe that will be the case in 2019.

Other investments

Our fixed interest and property allocations all performed as expected during the year. Our property investments produced an excellent return of over 12% through a combination of reasonable returns from our core unlisted investments and strong returns from some listed property holdings.

Going forward, both these asset classes look fairly unattractive. Income from fixed interest remains low. Property yields are the lowest we’ve seen for a very long time, and prospects for rental growth aren’t great for most property assets. We’ve mostly limited our buying in both cases to listed investments where we can buy at a discount to underlying value, but these opportunities are limited.

Current Portfolio and 2019 Outlook

To paraphrase John Kenneth Galbraith and with apologies to any economists reading this, we believe there are two types of market forecasters:

- Those who don’t know; and

- Those who don’t know they don’t know.

We are certain that we don’t know what will happen next, and we pay very little attention to macroeconomic and market forecasts. Instead, we spend that time assessing current valuations compared to long term averages, recent performance, investor sentiment and market risks. Our asset allocation must always be diversified, but it also incorporates our view of asset class valuations and return prospects, both in absolute terms and relative to each other and the opportunities available. Put simply, we will hold more investments in areas where we feel values are cheap and opportunities abundant, and less where the opposite is the case.

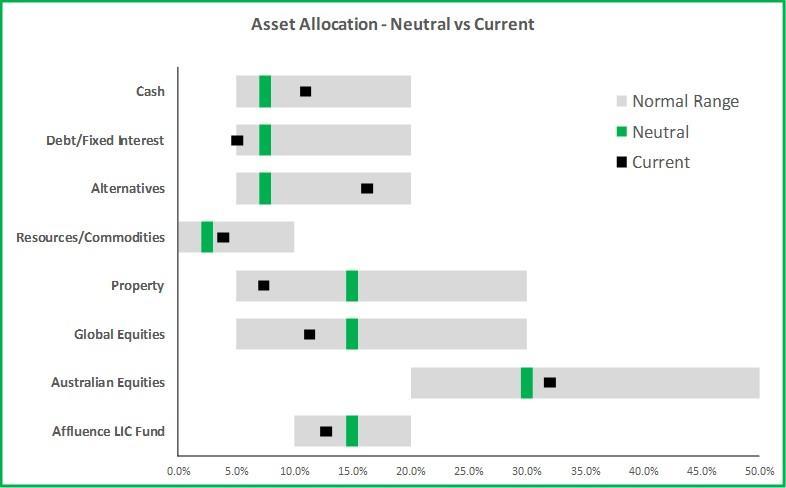

As at 31 December 2018, our asset allocation was as follows:

Below we’ve explained our positioning in a little more detail.

Equities

We believe that on average Australia equities are currently around fair value. However, there is a large variance in equity prices between very cheap and very expensive. Some of our Australian managers have had a very difficult 2018. The good news is that these managers are now seeing exceptional value in their portfolios. We have increased our allocation to these managers as the opportunity has increased, and we are excited by the prospects over the next couple of years.

We have been underweight global equities virtually since inception of the Fund. This has been particularly driven by our belief that US equities have been far above fair value. To date this has hindered the fund, as US equity returns have been exceptional (even with the recent fall). Notwithstanding the market correction, we continue to have limited direct exposure to US equities as we still believe they are one of the most overvalued asset classes. Through our global asset managers, we have been increasing our exposure to Emerging Markets and Asia, as we believe they offer superior relative value. However, we still remain relatively underweight.

Our Affluence LIC Fund also provides access to a range of LICs investing mostly in Australian and Global stocks, although increasingly we can also access alternative investment strategies and asset classes through LICs. This is an important part of our portfolio and one in which we believe we have an advantage via our discount capture strategy.

How our equities allocation changes in 2019 and beyond will very much depend of where markets go. But if stock markets fall further, expect us to have more exposure to equities. And if they rise substantially, we are likely to sell down part of our holdings.

Property

Our property allocation has reduced from approximately 20% three years ago to around 7% now. Cap rates (the cash yield derived from the asset) are now well below the pre-GFC period, and the value being paid for assets on average is well above replacement cost. We started our careers in property funds management and we love property. But we cannot come up with a compelling rationale to explain current values and their implied return prospects over the medium term.

Commercial property is notoriously cyclical, and while we have no idea what the catalyst may be that causes the reversion to the mean, we still believe in property cycles. We expect our property allocation to stay around the bottom end of our range unless we see the opportunity to buy at more reasonable valuations.

Fixed Interest

There are two main sources of interest return from fixed interest/bond investments:

- Risk free rate – Essentially investors need to be paid in order to lend money. Government bonds of highly rated countries such as US and Australia are considered to reflect the risk free rate, presumably because there is no risk of default. While current bond rates are above the all time lows from a couple of years ago, they are still incredibly low. For example, the current Australian 10 year bond yield is a miserly 2.3%.

- Credit risk premium – This is the premium investors need to be paid in excess of the risk free bond rate to compensate for the risk of not being repaid. Again, while not at all time lows, current credit spreads are well below historical averages, while at the same time the average credit rating and credit quality are declining. This translates into a situation where investors are getting paid less to accept more risk.

Our current fixed interest allocation is at the very bottom of our range, weighted towards credit exposures. We do not have any significant government bond exposure, as the returns are insufficient. We continue to seek additional opportunities in this sector that have a reasonable risk versus return profile, however expect to remain near the bottom of our range in the short to medium term.

Alternatives

As discussed earlier in this letter, we have increased our allocation to alternatives over the past 12 months. Our current allocation at over 16% is well towards the upper end of our range. This higher allocation is largely because most other defensive assets are somewhere between expensive and extremely expensive. Over the medium to long term we are targeting a return of at least our benchmark for this sector. While recent performance has been below this return target, we remain confident of these strategies and the underlying managers running them.

Risks

There are always risks in investing. We try to be mindful of macro risks, however usually the ones that hurt the most are those that almost no one had anticipated. We believe the best defence against macro risk is exceptional diversification. And we believe the biggest determinant of risk in any investment is the price you pay for the asset. No asset is so good that there is no price too high, and there are very few investments so bad that there is no price too low.

Here are a few of the current major risks in the world that may or may not cause issues:

- For much of the past 10 years post GFC central banks have been flooding markets with liquidity through quantitative easing. This has recently started to reverse, with quantitative tightening occurring and sucking liquidity out of the market.

- Interest rates are rising (especially in the US).

- There are many governments, companies and individuals that are carrying huge levels of debt, in many cases higher than pre-GFC. This could become more of an issue as interest rates rise.

- Global trade wars and a China slowdown could do a lot of damage.

- Falling house prices in Australia.

All the risks above are widely known. For such risks, markets have priced in a greater negative impact than can ultimately be expected. An uncertainty premium. That doesn’t mean it can’t get worse, but it does mean the more everyone is talking about the potential for bad things to happen, the more value is likely to be apparent. Rather than worrying about the bad things that everyone is talking about actually happening, you should be more worried when markets are roaring ahead, investors are carefree, and you hear the dangerous phrase “its different this time”.

Summary

The past 12 months performance has been disappointing, but it’s a normal part of the investment cycle. The good news is that our underlying portfolio looks more attractive than it has for some time, which makes us feel very positive about the prospects for the next few years, notwithstanding the potential for more bumps along the way.

Ourselves and our families are some of the largest unitholders in the Fund and as managers, we charge only a performance fee on positive performance (after recovering any negative performance first). We will always do what we think is best in order to maximise long term performance.

We would like to thank you for your continued support and your trust.

If you have any questions, you’re more than welcome to contact one of us at any time.