This article was originally published on Livewire.

As we approach the end of 2024, it appears that the market for Listed investment Companies is somewhat capitulating. Even LICs that have done everything right, performed well and historically traded at par or a premium are falling into discounts. There is certainly no fundamental reason for it, but rather it appears to be part of the current larger irrationality of markets.

It is not just LICs that are under pressure, but pretty much everything that is not in a large cap index. For the last 3 years the total cumulative returns for the ASX200 Index were +31.5%, the ASX Small Ords -0.2%, and the ASX Emerging Companies Index -7.5%. Markets continue to become more irrational every day. The valuations of equities powering the larger indices are at nosebleed levels (such as CBA at more than 25 times falling earnings), while many small and microcap stocks are very cheap. We believe this is an incredible opportunity for patient investors, but for us it has been a frustrating period as we await commonsense to make a comeback.

Our thesis for the current market is that it is stuck in a ‘liquidity flywheel’. The concept of a liquidity flywheel was explained very well in an LT-3000 Blog post from July 2020:

“A liquidity flywheel is a situation where inflows into an asset class lead to buying pressure that pushes up prices, leading to favourable apparent return and volatility characteristics in the said asset class. This favourable outcome then attracts yet more inflows, leading to yet more buying, etc. Conversely, poorly performing asset classes with significant downside volatility can lead to investor redemptions, leading to forced selling that contributes to yet further price declines, yielding even worse returns and even greater redemptions, and so on. This process can go on for years, and sometimes even for decades, and is a fundamental contributor – perhaps the most important contributor – to both major asset-class bubbles, as well as asset price busts and secular lows that lead to fire sale prices (which are ‘anti-bubbles’ driven by the same drivers of bubbles in reverse).”

This definition explains how a company such as CBA can reach $160 per share, even though most sell side analysts have a price target closer to $100 per share. It also explains, through ‘anti-bubbles’, how assets such as LICs can go from ‘reasonably priced’ to ‘crazy cheap’.

Current LIC Market

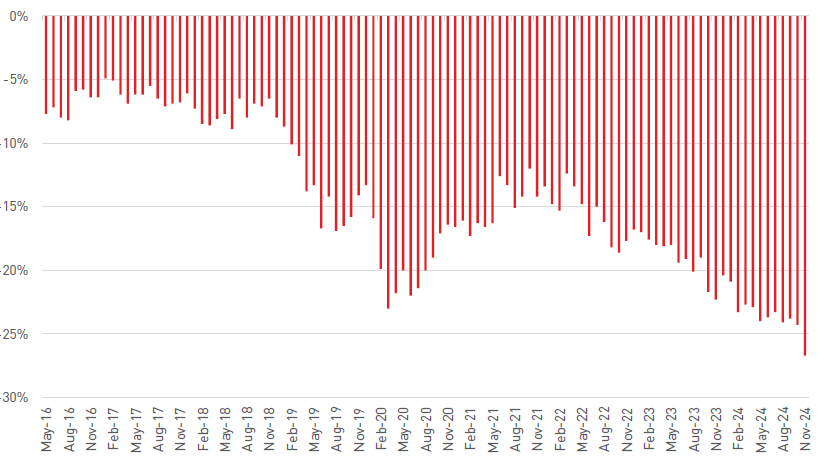

Discounts to NTA across the sector are at decade highs. The largest LIC in the market, Australian Foundation Investment Company (AFI), has recently been trading at a greater than 10% discount. This is almost unheard of. On average it trades at par to a small premium.

Apart from the momentum effect of ‘liquidity flywheels’ described above, other possible reasons for the increase in discounts to NTA include:

- Growth in exchange traded managed funds. The last few years has seen an explosion in the number of these traded funds. Previously, these types of structures were only used by index tracking strategies. Now, they are used for Australian and global share strategies, including hedge funds and more alternative strategies. These funds have measures in place to ensure they always trade within a close range of NTA, thereby eliminating the discount risk (but also the potential additional returns for active investors who can buy well). These ETF structures work for liquid assets, but for more illiquid assets and other strategies that require a stable pool of capital, they are not appropriate.

- Increase in interest rates. Many retail investors own LICs for the consistent payment of dividends. With the increase in interest rates over the past couple of years, investors can earn a similar level of income in fixed income investments without taking on the additional equity and discount risk. We expect this trend to reverse when the RBA first starts to cut interest rates. Right now, that looks like it will be sometime in the first half of 2025.

- Passive investment growth and active management underperformance. The current irrationality of markets has made conditions particularly hard for active management. The recent trend of expensive assets becoming more expensive as cheaper assets become cheaper goes against many active managers processes. However, as an increasingly large proportion of investment flows goes to passive strategies that are blind to valuations and fundamentals, this leads to further passive outperformance. The vast majority of LIC managers are at least somewhat active, thereby the recent underperformance has further hurt the sector.

The current level of discounts across the sector is unsustainable. While the timing and catalyst are unknown, there is too much capital tied up in the LIC sector for this type of inefficiency to continue indefinitely. It is likely the current trend of some windups, consolidations and delistings will continue, both voluntary (led by LIC managers) and forced (led by LIC shareholders).

There are suggestions that LICs are now unviable and unsustainable moving into the future. That is music to our ears. Usually, when investors declare an asset class uninvestible, or finished for good, it’s a classic sign a bottom is nearby. Even if this was true then this represents a tremendous opportunity for investors to profit over the next few years while the sector winds down and discounts are eliminated through realisations.

At current levels, even if discounts never close, you are buying one dollar of value for 75 cents. This has the added benefit of multiplying the investment returns generated by the LIC manager. For example, an 8% underlying investment return on a $1.00 NTA is equivalent to a 10.7% return if you only paid $0.75.

LIC Director Inaction

For many LICs, the Board of Directors is stacked with friends and associates of the manager. Many LICs trumpet the fact that they have a majority of external non-executive directors. This does not always help shareholders unless the Directors are determined to think and act independently of the manager. Many Boards have proven to be exceptionally inactive in dealing with three main issues in the LIC sector:

- Raising equity at a significant discount to NTA. This is one of the greatest sins an LIC Board can commit. The reasons given to justify a discounted capital raising (say more than a 5% discount to NTA) are always amusing, and mostly irrelevant. Examples such as being able to take advantage of excellent investment opportunities, increased liquidity or lowering the overall cost ratio of the company are often given. Unfortunately, the benefits of these factors are usually insignificant, compared to the value destruction brought upon existing shareholders by raising at a discount to NTA. They never mention the real reason it’s attractive, which is to increase the FUM and therefore increase the fees payable to the investment manager.

- Investment manager not performing. Manager underperformance is not a straightforward issue, as market conditions, liquidity flywheels, contracted terms and many other factors play a part. However, there are certainly LICs which have significantly underperformed their stated objectives over the medium to long term. A board acting in the best interest of shareholders would deal with these types of issues. However, this very rarely occurs.

- Dealing with persistent discounts. There always needs to be some allowance for overall market conditions. For example, at the moment the majority of the sector is trading at discounts well above their average, and even those LICs that often enjoy a premium have fallen to a discount. However, there are some LICs that have continually traded a 15% plus discount for more than 5 years. It certainly appears that for some LICs, discounts become “engrained”. No matter if performance is excellent or marketing is increased, they have a discount level they trade at. Directors have options available to deal with persistent discounts, but in the vast majority of cases, they put in place a token share buyback and talk about increased marketing efforts, rather than taking the harder options of delisting, winding up, or at least letting shareholders vote on these options.

2024 Corporate Actions

The last 12 months has seen the following corporate actions in the LIC market. In each case, the solution has, or will permanently eliminate the NTA discount:

- Partners Group Global Income (PGG) – delisted and became an unlisted trust.

- NB Global Corporate Income (NBI) – delisted and became an unlisted trust.

- Magellan Global Fund (MGF) – delisted and became an unlisted trust.

- Forager Australian Shares (FOR) – delisted and became an unlisted trust.

- QV Equities (QVE) – merged with WAM Leaders (WLE).

- Platinum Capital (PMC) and Platinum Asia (PAI) – expected to merge with their respective exchange traded managed funds in 2025.

This follows on from quite a few others in the couple of years before that.

For the most part, these Boards of Directors and Managers have shown they care about their shareholders, and have taken action, even though it is likely to lead to reduced revenues for the managers. In some cases, they have needed some gentle (or not so gentle) persuasion from shareholders.

For those LICs that have continually traded at 15% plus discounts over the long term, it is likely that the board and manager are not going to voluntarily prefer the LIC shareholders interests over their own. Otherwise, they would probably have done so already.

The most likely catalyst for action in these LICs will be shareholder pressure, including from activist investors. We have written about the significant activist investor interest in the sector over the past 18 months. It is surprising that this has so far led to no specifically targeted campaigns to deal with these discounts. It is unclear what they are waiting for, as it is difficult in many cases to see how they would not be successful in either winding up or converting the LICs, were shareholders given the opportunity to vote on such a proposal.

It is certainly possible that once the first campaign starts, others will follow. Perhaps then the boards of other LICs will be shocked into action.

Conclusion

There is no doubt that the buying in the LIC sector at the moment is exceptional. Owning assets at a discount is accretive even without the discounts closing. Owning assets at a discount plus some reversion to the mean is a very powerful combination for outperformance. There is no guarantees that discounts can’t move out further, but the elastic band can only stretch so far before springing back.

This is a once in a cycle investing opportunity in the LIC sector.

This is strengthened by the ability to bias a portfolio towards those LICs that invest in sectors that have substantially lagged the greater market, and are currently cheap before applying the LIC discounts.

Want to know more?

We encourage you to do your research before investing in any LIC. If you would like to learn more, here are some of other articles on LICs:

Download the Affluence LIC Guide

Building a diversified portfolio using LICS

Disclaimer

This Fund Profile was prepared by Affluence Funds Management Limited (Affluence). It was prepared to assist investors in various Affluence funds in understanding the investments of the relevant Affluence fund in more detail. It is not an investment recommendation. Prospective investors are not to construe the contents of this article as tax, legal or investment advice. Neither the information nor any opinion expressed constitutes an offer by Affluence, its subsidiaries, associates or any of their respective officers, employees, agents or advisers to buy or sell any financial products nor the provision of any product advice or service.

This Fund Profile does not take into account your objectives, financial situation or needs. In deciding whether to acquire or continue to hold an investment in any financial product, you should consider the relevant disclosure documents for that product which are available from the product provider. Affluence recommends you consult your professional adviser before making any decision to invest.