Introduction

It feels like we are stuck in the twilight zone. In 2023, investors oscillated between believing inflation was sticky and economies were heading for trouble, and the perfect scenario where central banks had engineered a beautiful ‘soft landing’ with inflation falling back to target and economies continuing on their merry way. At the end of October the ASX200 Index was flat for 2023. Then a 12.3% increase in the last two months of the year led to an impressive CY23 return of 12.4%. In the US, the S&P500 Index finished the year up an incredible 26%.

As we have said previously, we believe the investment world changed in January 2022 when the spectre of higher interest rates entered investors minds. Over the last two years, central banks have increased interest rates substantially; the RBA from 0.1% to 4.35%, the US Fed from 0% to 5.375%, and the UK Central Bank from 0.1% to 5.25%. These have been some of the fastest interest rate increases in history.

Central banks raise interest rates to increase the cost of capital, reduce aggregate demand, increase unemployment and slow down the economy. However, despite these rapid increases, global economies have remained remarkably resilient. Economists are now putting this down to the massive household savings buildup from Covid related government stimulus. This cash buffer has allowed households to continue to spend strongly, even in the face of rising inflation and increased debt costs. As a result, the normal pattern of increasing unemployment and a slowing economy has not yet occurred.

And here is the conundrum. Despite these big interest rate increases, Australian and global equity markets are at or near their all-time highs. Investors are effectively saying that interest rates increasing from zero to 4-5% in less than 2 years is not important. US equity valuation levels are back to being amongst the most expensive in history. US equity markets are pricing in earnings growth (increasing company profits) for the next two years of 11% and 12%. This is well above the last 20 years average. To us, pricing above average earnings growth into an environment where the lag from previous interest rate increases is still occurring, seems extremely optimistic.

While central banks have recently started to acknowledge that there is potential for interest rate cuts, markets are assuming much more aggressive falls than indicated by central bankers.

Equity markets are pricing in the Goldilocks scenario whereby:

- Central banks have completed their rate increasing cycle.

- Inflation has been defeated and will reduce to central bank targets.

- Economies will continue to be resilient, with very little chance of a recession.

- Central banks will therefore be able to aggressively reduce interest rates.

- Falling interest rates will be good for the economy and asset prices.

In simpler terms, markets are priced for perfection. If actual events don’t turn out to be perfect, then current valuations will likely end up being too optimistic.

We’ll happily take the Goldilocks result. But we are preparing for the porridge being either too hot (inflation proves sticky and rates stay high for longer) or too cold (the slowdown happens, which lets rates fall, but also impacts company earnings). In anticipation of this, we are positioning portfolios for a range of potential scenarios.

Opportunities

It’s not all bad news. While the major indices are near all-time highs and reflect poor value on average, there are significant pockets of attractive opportunities:

- Fixed Income. Most fixed income investments have had the benefit of the RBA increasing the cash rate from 0.1% to 4.35%. It is now possible to construct a diversified portfolio that yields 7-8% with substantially less risk than equities. It’s such an attractive opportunity set that we have launched a new fund, the Affluence Income Trust, just to take advantage of it.

- Equity Small Caps. Basically, the smaller the company, the more it is being ignored by the market. While this statement is generally true in all market conditions, currently this phenomenon has gone to extremes. The performance gap between large caps and small caps is at historical limits. We expect small and microcap stocks to deliver very attractive returns over the medium term, and to significantly outperform large caps.

- LICs. Investors continue to shun LICs. As a result the discounts available are amongst the highest in history. Part of the reason is the popularity of Exchange Traded Managed Funds (ETMFs). These have the benefit of being bought and sold on the ASX like an LIC, without the discount. Given the large discounts on offer, there has been an increase in activist investors taking positions in the sector. This is likely to result in a number of forced capital events which should result in strong return for investors.

- REITS. Many REITS have recovered from cyclical lows to some degree over the last two months, but they remain well down over the past two years. There continue to be some excellent individual opportunities.

- Resources. This is more of a medium-term opportunity. If a global recession does occur, resources are likely to be punished. But over a longer time period, we believe that many commodities will experience a fundamental supply shortfall.

Investment performance

It’s worth remembering that for all our strategies, our focus is always on three things:

- Delivering better than average returns over three years and longer.

- Limiting the impact of market corrections and thus avoiding significant long term capital losses.

- Providing a decent level of regular income, with the option to reinvest and compound returns.

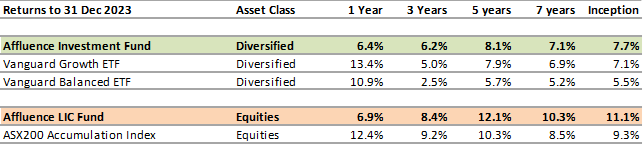

The below table summarises the performance of two Affluence Funds over their lifetime.

Both Funds underperformed in CY23. They both outperformed over the first ten months of the year, but did not keep up with the aggressive risk on rally over the last two months. We don’t expect to keep up with equity markets when they move rapidly higher. By design, our portfolios have significantly lower market risk than the ASX 200. Our philosophy to achieving superior long-term returns is to limit the impact of market drawdowns, and invest more aggressively when markets are cheap and there is more return potential for less risk.

Our longer-term returns compare very well with passive alternatives. More importantly, we are much more excited about the value embedded in our fund portfolios, compared to the markets in general. This provides us with an excellent starting point for the medium term.

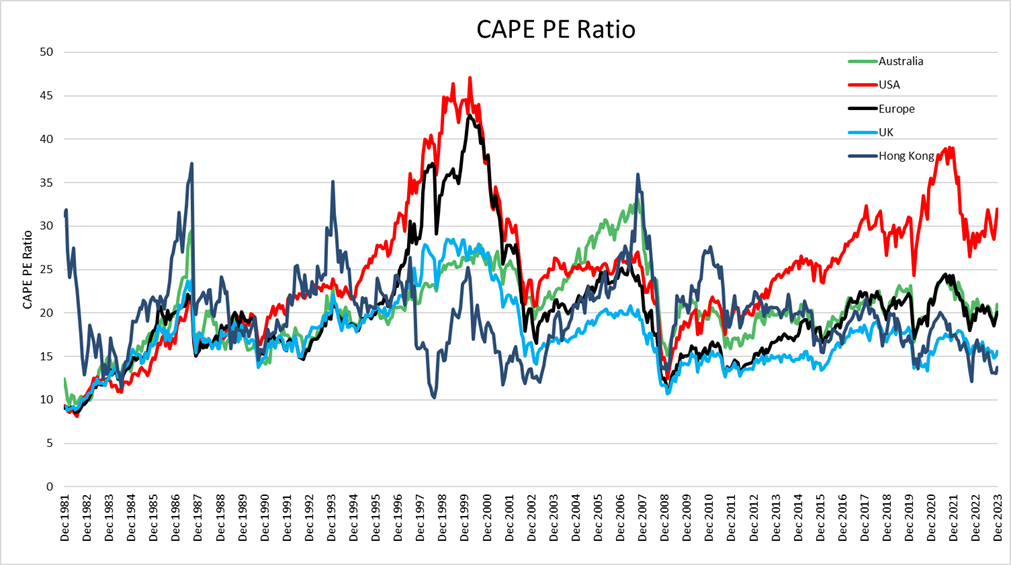

CAPEs & profit margins

One reasonable guide to market valuations that we pay attention to is the Cape Shiller 10 year PE ratio. This differs from a standard PE ratio, in that it uses the average of the previous 10 years earnings adjusted for inflation. This is intended to normalise for abnormally high or low earnings through market cycles. We believe this is particularly relevant at the moment, as US profit margins are well above average, and likely not sustainable.

The graph below shows the CAPE PE ratio since 1981 for Australia, the US, Europe, the UK and Hong Kong.

The US CAPE PE Ratio is below the frothiest part of the recent bubble in 2021. However it remains well above long term averages and we would expect poor long term returns from this starting point. US equity markets continue to assume strong earnings growth in 2024. We are about two years into the US Fed tightening cycle. Historically this is when the full impacts of increased interest rates start to bite.

Australian and Europe valuations are only a little above average. Given there is still a reasonable possibility of a recession, this does not give us much comfort.

The old adage that when the US sneezes Australia catches a cold is a concern. If the US market reprices closer to historic averages, there is a real risk it drags global markets with it.

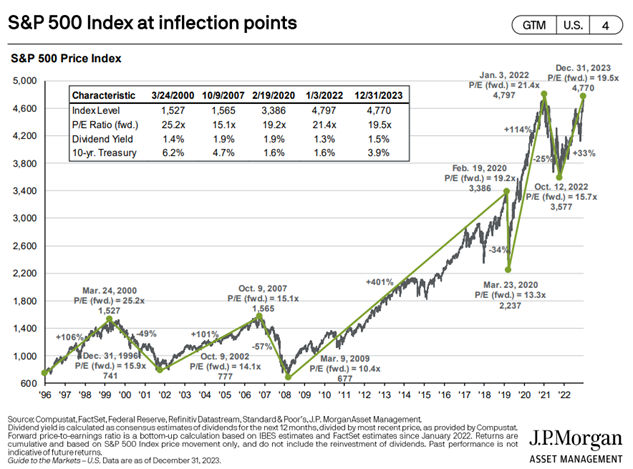

The graph below compares the US S&P 500 Index now, to some recent market peaks.

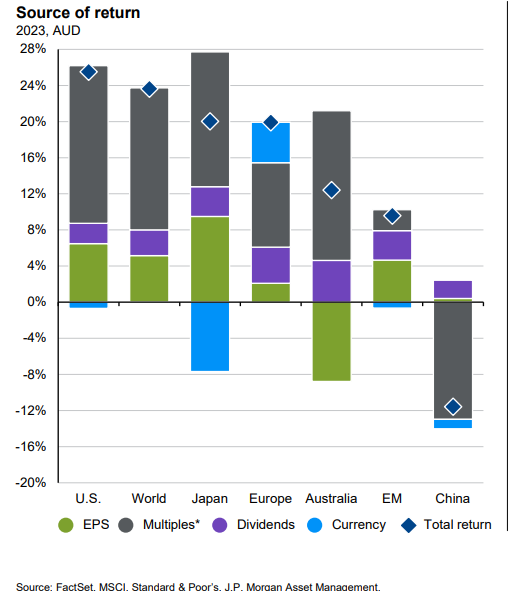

Finally, the following graph shows the source of returns for global markets in 2023. It’s a little complicated, but the important element is that the major driver of performance in 2023 was an expansion of the earnings multiple (the grey bar). This is especially true for the US market. This indicates that markets didn’t increase due to, for example, higher earnings. Rather, investors just decided they were happy to pay more for the same income stream.

Portfolio Positioning

Given our cautious outlook, we have positioned the portfolios with a balance between investing in growth assets we believe are undervalued, and alternative and fixed income defensive assets we believe will outperform in more difficult market conditions. This includes:

- Some hedging to soften any market falls.

- Very limited US equity exposure.

- A strong value style bias with limited growth style investments.

If further downside occurs, we believe we are reasonably positioned to ride out the turmoil. In this scenario, we would hope to perform substantially better than equity markets.

If markets have already bottomed, we would expect to be well positioned to deliver decent returns over the next 3-5 years.

Which Affluence Fund to choose?

We are often asked by new investors which of our funds they should invest in. We’re not allowed to give personal investment advice, so it’s a question we can’t answer directly. Instead, we prefer to highlight the return target and expected risk profile for each of our funds. It’s then up to you to decide (along with your advisor if you have one) where you allocate your investment capital. This is likely to be heavily influenced by your return expectations, your risk tolerance and your investment timeframe.

Our newly launched Affluence Income Trust targets a minimum distribution equal to the RBA Cash Rate plus 3% per annum paid monthly, while preserving capital over rolling 3 year periods after payment of those distributions. The Fund is currently paying distributions at the rate of 7.5% per annum, from a highly diversified portfolio of fixed income assets. We aim for this to be our lowest risk Fund. The recommended investment period is a least 1 year.

The Affluence Investment Fund targets a return of inflation plus 5% from a very diversified mix of investments. In addition, this Fund aims to pay monthly distributions and perform much better than stock markets, particularly the ASX200 Index, when markets fall. In both risk and returns, this Fund sits somewhere well above cash and bonds but below equity markets. It has a medium risk profile and the recommended investment period is a least 3 years.

The Affluence LIC Fund targets equity-like returns. We aim to beat the ASX200 Index returns with less volatility. You should assess the LIC Fund as having a similar risk/reward profile to an equity fund, although we believe the current level of discounts for LIC’s provide a very attractive entry point for this Fund. The recommended investment period is a least 5 years.

The Affluence Small Company Fund targets the potentially higher returns available from smaller companies. It has the highest potential returns, and the highest risk of all our funds. Currently, this fund is only available to wholesale and sophisticated investors, though we hope to be able to change that in time. If you’d like to learn more about this fund, or to register your interest should it be available to all investors in the future, let us know.

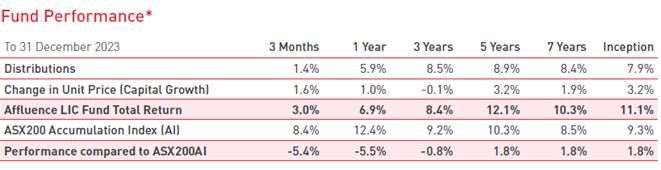

Affluence LIC Fund Performance

The Affluence LIC Fund has continues to outperform its benchmark (ASX200 Index) over 5 years and longer, with significantly lower volatility.

For CY23 the Fund increased 6.9%, compared to 12.4% for the ASX200 Index and 7.8% for the ASX Small Ords Index. The Fund outperformed over the first ten months of the year, however increased only 5% compared to the 12.3% over the last two months. This is not unusual for LICs, which tend to follow the market with a lag.

We have previously discussed our scepticism about the durability of the November/December market rally. However, whether the market powers on from here or suffers speed bumps ahead, we believe that the LIC portfolio has great potential to outperform over the next few years.

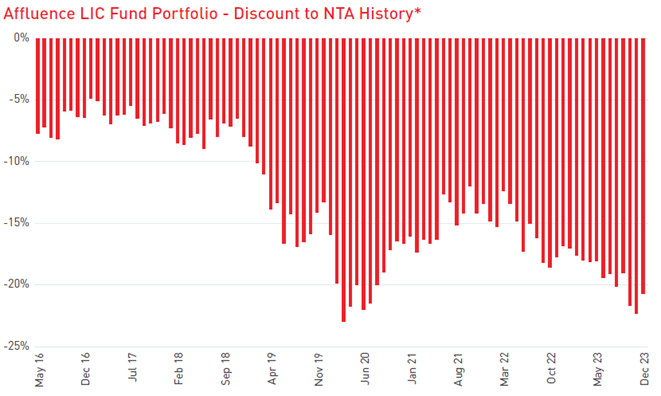

The average discount to NTA for the portfolio increased from 16.8% at 31 December 2022 to 21% at 31 December 2023. As the above chart shows, discounts have been consistently increasing from mid-2002. While this has obviously been a headwind to performance over this period, we find this incredibly exciting as we look forward.

Over the past 12 months the following corporate transactions have been announced in the LIC sector:

- EAI – Ellerston Asian Investments. Was converted from an LIC into an ETMF after a prolonged period of trading at a substantial discount to NTA.

- PGG – Partners Group Global Income Fund. Listed Investment Trust that converted to an unlisted trust after sustained trading at a discount.

- MGF – Magellan Global Fund. After sustained activist pressure and potential legal action, the manager has announced they are working on a mechanism to convert from an LIC to a structure that will allow investors to exit at close to NTA.

- FOR – Forager Australian Shares Fund. FOR originally started as an unlisted trust, before listing in 2016. After a prolonged period of trading at a discount, the manager made the admirable decision to convert from an LIC to a structure that will allow investors to exit for close to NTA.

- NBI – NB Global Corporate Income. Similar to PGG, this LIT is currently undertaking a transaction to convert to an unlisted trust.

In addition to these announced transactions, there are a number of activist investors who have taken substantial positions in various LICs and will likely be agitating for action. In particular, Saba Capital from the USA are well known for taking aggressive, hostile action. They have taken positions in the following LICs:

- VG1 – VGI Partners Global Investments

- HM1 – Hearts and Minds Investments

- PIA – Pengana International Equities

The current level of discounts available in the LIC market are simply unsustainable. Through a combination of forced corporate windups from activist investors, and the realisation from retail investors of the opportunities currently on offer, we expect the overall discounts to NTA to decrease over the medium term. This can be a tremendous benefit to the Affluence LIC Fund.

Affluence LIC Fund Positioning

Somewhat paradoxically, given our assessment of elevated market valuations, we enter 2024 fully invested. Even more surprisingly, a large part of our purchases were made during the last two months of the year, when markets rallied. In November and December we were able to purchase a number of LICs that had not yet reacted to the market movements, including some that were at 12 month lows.

We have increased our holding of index market hedges as a result. This has allowed us to take advantage of the excellent discounts on offer, while still giving the Fund some protection if markets do fall.

Overall, we own a portfolio of LICs trading at more than a 20% discount to NTA, many of which are also held by activist investors. A significant portion of the LICs we own are focused on small and microcap stocks. The smaller end of the market has significantly underperformed the larger caps, and we believe that the value on offer is fantastic. We are very confident that over time the overall discount to NTA will decrease, which can help to produce strong returns for the portfolio.

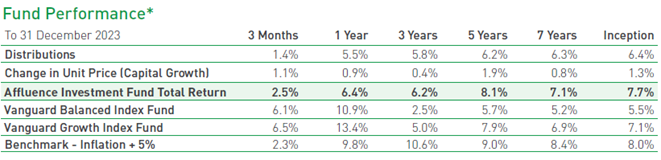

Affluence Investment Fund Performance

The Affluence Investment Fund performed reasonably in 2023, though again missed out on much of the short erm recovery in the last 2 months. While the Fund underperformed the passive alternatives over 12 months, it remains well in front over the suggested minimum investment period of 3 years and longer. The long term return of 7.7% remains adequate, however we believe the current portfolio shows significantly more potential than historic returns would suggest.

Affluence Investment Fund Positioning

It is impossible to build a portfolio that can navigate market downturns and then keep up with aggressive market rallies. Investing is always a balance between offence and defence. Our job is to ensure we strike the right balance to achieve our return target over the medium to long term. In doing this, we seek to limit the downside relative to the major asset markets and then recover those losses more quickly.

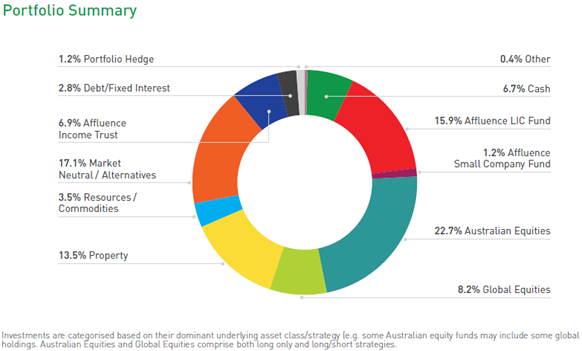

At 31 December 2023, the Fund portfolio looked like this.

Over the past 12 months we have made the following significant changes to the portfolio:

- Fixed Income. Increased our allocation, including a 7% allocation to the Affluence Income Trust. Given current interest rates, we believe we can achieve returns that are close to long term equity averages, with relatively low risk.

- Alternatives. We classify alternatives as investments that have little to no direct impact from equity markets. We have added to these investments where we believe they should be able to generate reasonable returns regardless of equity market movements.

- Property – We increased our allocation to REITs during the year after they were aggressively sold off. REITs rallied over the last two months of the year as bond rates fell, however there continue to be attractive opportunities in the A-REIT market.

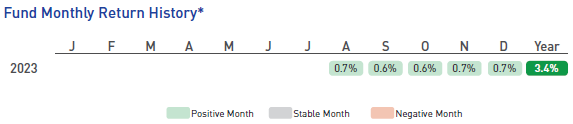

Affluence Income Trust Performance

Though we only formally opened the Affluence Income Trust for investment in January 2024, the Fund has been operating and investing since July 2023. It is focused purely on delivering attractive monthly income. Though the performance history is very short, performance to date is in line with our goals.

Affluence Income Trust Positioning

The Fund has a very flexible investment mandate within the fixed income asset class. Importantly, this allows us to take advantage of what we believe to be the best risk adjusted investment opportunities within this asset class at any given time. This is very rare in the fixed income sector, with most funds constrained to investing in a single sub sector.

The Fund portfolio currently includes a range of investments chosen by us, including access to many exceptional fixed income specialists normally only directly available to wholesale and institutional clients. For most individual investors, it would be very difficult to build such a diversified portfolio of fixed income assets.

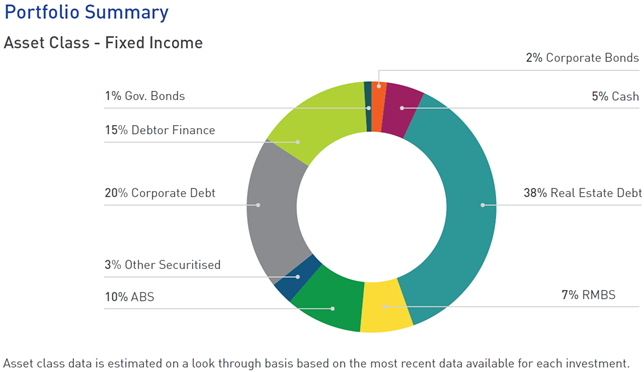

At 31 December 2023, the Fund portfolio looked like this.

Some examples of the types of investments in the Fund at the moment include:

- Commercial Real Estate Debt. Investments that derive their returns from lending to real estate borrowers. The type of assets borrowed against include office and industrial buildings, shopping centres, undeveloped land, construction projects and farmland.

- Private Credit Loans. Investments that derive returns from lending to corporate borrowers. The borrowers are typically too small to access the listed corporate debt markets, and with banks reducing their lending appetite, specialist private credit lenders are filling the void.

- Asset backed securities. RMBS and ABS loans are securitised facilities where thousands of individual loans are bundled together. The major banks typically finance the largest highly rated tranches, while specialist asset managers invest in the subordinated tranches.

- Traded debt securities. These investments are usually debt securities issued by either governments or major corporate borrowers, and are liquid and highly traded.

We are excited by the depth and breadth of opportunities available in the fixed income sector. For as long as the cash rate stays at or around current levels, very attractive returns are possible with reasonably low risk.

After pretty much avoiding the sector entirely while interest rates were extremely low, we now expect fixed income to be a key source of attractive risk adjusted returns for some time. You can read more about the opportunity in fixed income here.

Thank you to all of you who trusted us with your hard earned capital during the year. It is a responsibility that we never take for granted. We look forward to continuing our search for exciting investment opportunities in the coming years.